The “bunker“, which is the main consumable for ships, is Fuel Oil obtained by the distillation of crude oil. Crude oil contains sulfur, which causes harmful emissions after combustion in ship machinery. Sulfur oxides (SOx) are extremely harmful to human health. It is known to cause respiratory distress symptoms and lung diseases. SOx in the atmosphere contributes to acid rain that can harm all living creatures, crops, forests, all kinds of water basins, as well as those living in these waters, without minding wild or modern.

In general, limiting SOx emissions caused by the use of fossil fuels will increase the air quality in the atmosphere and protect living things and the environment.

IMO regulations to reduce sulfur oxide (SOx) emissions from ships first came into force in 2005 under Annex VI of the International Convention for the Prevention of Pollution from Ships (known as the MARPOL Convention). Since then, the limitations on sulfur oxides are getting stricter.

Simply put, limiting sulfur oxide emissions from ships reduces air pollution and provides a cleaner living environment. The reduction of SOx also helps to reduce the small harmful particles that are generated when fuel is burned.

IMO monitors the sulfur content of fuel used in ships globally. The latest figures show that the annual average sulfur content of residual fuel oils tested in 2017 was 2.54%. In 2017, the worldwide average sulfur content for distillate fuel was 0.08%.

Since 1 January 2015, the sulfur limit for Fuel Oil used by ships operating in the Emission Control Areas (ECA) designated by IMO for the control of sulfur oxides (SOX) has been 0.10% m / m. ECAs for SOx created under MARPOL Annex VI are: Baltic Sea region; North Sea region; North America region (includes designated coastal areas other than the United States and Canada); and the United States Caribbean Sea region (waters around Puerto Rico and the US Virgin Islands).

Since 1 January 2015, the sulfur limit for Fuel Oil used by ships operating in the Emission Control Areas (ECA) designated by IMO for the control of sulfur oxides (SOX) has been 0.10% m / m. ECAs for SOx created under MARPOL Annex VI are: the Baltic Sea area; the North Sea area; the North American area (covering designated coastal areas off the United States and Canada); and the United States Caribbean Sea area (waters around Puerto Rico and the United States Virgin Islands).

The time IMO adopted Regulations to control air pollution from ships

IMO has been working to reduce harmful impacts of shipping on the environment since the 1960s. Annex VI to the International Convention for the Prevention of Pollution from Ships (MARPOL Convention) was adopted in 1997, to address air pollution from shipping. The regulations for the Prevention of Air Pollution from Ships (Annex VI) seek to control airborne emissions from ships (sulphur oxides (SOx), nitrogen oxides (NOx), ozone depleting substances (ODS), volatile organic compounds (VOC) and shipboard incineration) and their contribution to local and global air pollution, human health issues and environmental problems. Annex VI entered into force on 19 May 2005 and a revised Annex VI with significantly strengthened requirements was adopted in October 2008.

These regulations entered into force on 1 July 2010. The regulations to reduce sulphur oxide emissions introduced a global limit for sulphur content of ships’ fuel oil, with tighter restrictions in designated emission control areas. Since 2010, further amendments to Annex VI have been adopted, including amendments to introduce further Emission Control Areas.

Energy efficiency requirements entered into force in 2013.

IMO 2020

Until 31 December 2019, for ships operating outside Emission Control Areas, the limit for sulphur content of ships’ fuel oil is 3.50% m/m (mass by mass). The 0.50% m/m limit will apply on and after 1 January 2020.

The date of January 1, 2020 is set in the regulations adopted in 2008. However, a provision was adopted requiring the IMO to review the availability of low sulfur fuel oil for use by ships to help Member States determine whether the new lower global limit exists. IMO’s Marine Environment Protection Committee (MEPC 70), in October 2016, decided that the 0.50% limit shall apply from 1 January 2020.

What does the new limit mean for ships?

Under the new sulphur limit, ships will have to use fuel oil on board with a sulphur content of no more than 0.50% m/m, against the current limit of 3.50%, which has been in effect since 1 January 2012. The interpretation of “fuel oil used on board” includes use in main and auxiliary engines and boilers. Exemptions are granted in cases involving the safety of the ship, or saving lives at sea, or if a ship or its equipment is damaged. Another exemption allows a ship to experiment with the development of ship emission reduction and control technologies and machine design programs. This requires a special permit from the Flag State of interest.

How can ships meet lower sulfur emission standards?

Ships may have got engines able to burn different fuels that contain low or zero sulfur that meet the requirement of consuming low sulfur compliant fuel. For example, liquefied natural gas or biofuels.

An increasing number of ships are also using gas as a fuel as when ignited it leads to negligible sulphur oxide emissions. This has been recognised in the development by IMO of the International Code for Ships using Gases and other Low Flashpoint Fuels (the IGF Code), which was adopted in 2015. Another alternative fuel is methanol which is being used on some short sea services. 3 Ships may also meet the SOx emission requirements by using approved equivalent methods, such as exhaust gas cleaning systems or “scrubbers”, which “clean” the emissions before they are released into the atmosphere. In this case, the equivalent arrangement must be approved by the ship’s Administration (the flag State).

IMO has adopted a MARPOL amendment to prohibit the transport of non-compliant fuel for propulsion or combustion on board a ship unless an exhaust gas cleaning system (“scrubber”) is installed on board.

Controlling the discipline

Implementation is the duty and responsibility of the Administrations (flag States and port / coastal States). Ensuring that the 2020 0.50% m / m sulfur limit is implemented consistently and effectively is a high priority. Ships must be issued an International Air Pollution Prevention (IAPP) Certificate from Flag States.

This certificate includes a section stating that the ship is using fuel oil with sulfur content not exceeding the applicable limit value documented on bunker delivery note or using an approved equivalent regulation. They could also use surveillance, for example air surveillance to assess smoke plumes, and other techniques to identify potential violations.

If the rules are not respected, sanctions are determined by individual parties of MARPOL as flag and port states. IMO does not set sanction penalties, its sanctions are up to each State Party.

What is IMO doing to ensure proper fuel availability?

Implementation is the responsibility of the Member States who are contracting Parties to MARPOL Annex VI. The decision by MEPC in October 2016 to affirm the effective date of 1 January 2020 (more than three years before entry into effect of the 0.50% limit) is intended, in part, to provide sufficient time for Member States and industry to prepare for the new requirement, Regulation 18 of MARPOL Annex VI covers both fuel oil availability and quality. As regards the availability of fuel, the regulation requires that each Party “take all reasonable steps to promote the availability of fuels conforming to this Annex and inform the Organization of the availability of compatible fuels at its ports and terminals.

Parties are also required to inform IMO when a ship provides evidence that suitable fuel is not available. IMO Global Integrated Transport Information System (GISIS) urged the Organization to inform the Organization about the availability of compatible fuels at its ports and terminals well before January 1, 2020 through the MARPOL Annex VI module. MARPOL Annex VI Rule 18.1.

Why are ships less harmful than other modes of transport?

Ships emit pollutants and other harmful emissions. But they also transport large quantities of vital goods across the world’s oceans, and trade by sea continues to increase. According to UNCTAD, in 2016, ships traded over 10 billion tons for the first time.

Therefore, ships have always been the most sustainable way to transport goods. Ships are getting more and more energy efficient. IMO regulations on energy efficiency are updating themselves to support the demand for greener and cleaner transport than ever before. A ship that is more energy efficient burns less fuel and causes less air pollution.

In some articles it is cited that only a few large ships emit much more harmful air pollutants than all cars in the world.

However, this worst case scenario does not take into account the amount of cargo carried by the ships and the relative efficiency. It is important to consider the amount of cargo transported and the emissions per tonne of cargo transported per kilometer traveled. Studies have shown that ships are the most energy efficient mode of transport compared to other methods such as aviation, road trucks, and even railways.

On the other hand, it is also important to remember that shipping is responding to the demands of large volumes of world trade. As the world trade volume increases, more ship capacity will be needed.

Ships are the largest engines on the planet, and almost the largest diesel engines in the world are found on cargo ships. These machines have over 100,000 horsepower, compared to a mid-size car around 300 horsepower. Large container ships can transport more than 20,000 containers, and bulk carriers can transport more than 300,000 tons of goods such as iron ore. Very powerful engines are needed to float ships of this size. It is important to calculate how much energy is used to transport every ton of cargo per kilometer. When you look at the relative energy efficiency of different modes of transport, ships are the most energy efficient. Ships therefore burn less fuel, are more energy efficient, less air pollutants, and their emissions are lower.

Can low sulfur fuels cause problems for ship engines?

All Fuel Oil intended for combustion on a ship must meet the required fuel oil quality standards as specified in IMO MARPOL Annex VI (regulation 18.3). For example, fuel oil must not contain any additives or chemical waste that endanger the safety of ships or adversely affect the performance of the engine.

IMO discusses how to identify potential safety issues related to fuel mixes. It is recognized that if these fuels are not properly managed, compatibility and stability issues can occur. If necessary, additional guidance can be developed for crew and ship operators.

The International Organization for Standardization (ISO) standard (ISO 8217) determines and circulates maximum and minimum international standards for fuels used in diesel marine engines and boilers.

A study commissioned by IMO for the “assessment of fuel availability” concluded that the refinery sector has the capacity to supply a sufficient amount of marine fuels with a sulfur content of 0.50% m / m or less and a sulfur content of 0.10 m.

Do small ships also have to comply with the sulfur limit?

Yes they do, MARPOL rules apply to all ships. Vessels of 400 gross tons and over sailing to ports or offshore terminals under the jurisdiction of other countries must have an International Air Pollution Prevention Certificate issued by the ship’s Flag State. However, ships of all sizes must use fuel oil that meets the 0.50% limit as of January 1, 2020.

Some smaller ships may be using a suitable marine distillate for their engines. Like the small vessels operating in predetermined emission control areas may use fuel oil that meets the 0.10% limit in these emission control areas for instance.

IMO 2020 Update: The Impact We See So Far (Agust 2020)

Now that the deadline for January 1 has come and gone, we wanted to share an update on the real-world implications of IMO’s mandate.

With steamship lines beginning to purchase low-sulfur fuel in early November 2019, there was definitely an increase in fuel surcharges. There were many speculative fears that fuel wages would double or triple, but that is currently not the case.

In the first quarter of the year, the dry cargo market suffered from the financial burden brought by IMO 2020. Since the charter rates are inversely proportional to the maximum 0.5% sulfur marine fuel prices in important bunkering ports, the increased fuel costs after IMO 2020 were not reflected in the freight rates. Charter rates for ships (T / C time charter $ / day) rose in direct proportion to VLSFO prices and / but freight gains fell.

In fact, there were no stable inrease in T / C ratios as well, temporary fluctuations were experienced. As the fuel price rose, it was seen that shipowners had to lower the daily charter rates of their ships to keep their voyage rates constant. However, over time, freight and T / C rates settle in direct proportion.

The availability of products, that will have to be used as the day-by-day approaches 2020, the refineries’ ability to produce these products, and the rhetoric that these fuels will be too expensive and even that most ships may supposed to consume MGO, all have affected the chemistry of the maritime industry. However, with this pessimistic state of mind, while a stable balance is not expected to be established in a short time, VLSFO prices have started to decrease rapidly. For example, between January 6 and January 17, the price of 0.5 percent sulfur-containing marine fuel (VLSFO) supplied to ships at the port of Singapore fell from $ 740.00 / mt to $ 645 / mt, down 12 percent. Fuel supplying sources have confused the fuel demanders and the maritime market in general with alternative practices. Equilibrium could not be mentioned in such a climate. It was surely unfair forcing the buyers get alarmed and causing them to buy fuel in a panic due to fuel shortage. However, it should not be too strange to experience these negativities, as these are known behaviors and attitudes displayed in transition periods.

This wind blew hard for a while. Some rushed without looking at the price, in order not to have a nightmare of not finding out the fuel, no matter expensive or not, while others expected the prices to drop to reasonable levels as soon as the panic calms down, till the prices settle at a new balance. Because, the managerial risks that the decision mechanisms will face and the scandals they will create within the institution come before losing money in some cases.

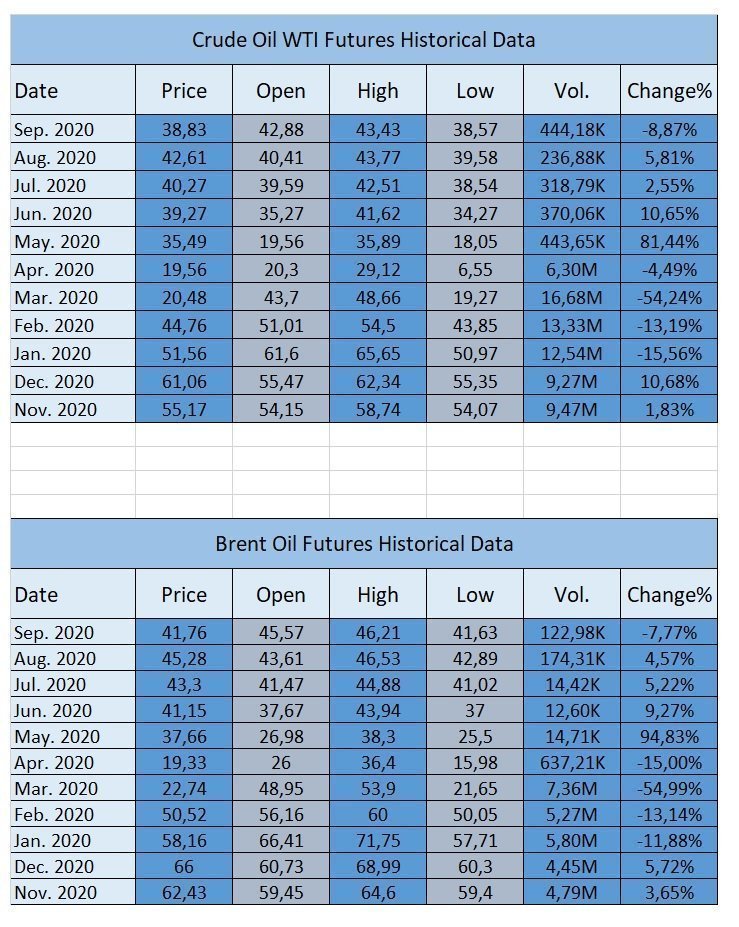

It’s time to take a look at the chart below before continuing to discuss the impact of IMO 2020 on the industry!

It is good to take a look at the status of two important international oil criteria since November 2019. Brent crude oil and US West Texas Intermediate (WTI) crude oil turned upside down. Nevertheless, the fearful prediction has not come true, the price of fuel also plumped. Unfortunately, this has not happened with a cooperation, contribution, ingenuity or victory of any industry.

While the world’s leading oil producers, exporters, importers, consumer countries bullied each other with the geopolitical advantages granted by the world at the end of 2019 and early 2020, while the endless conflicts of various superiority and interests of the muscular world countries continue, a health monster that says I am coming in the last quarter of 2019 It affected the realm. As of March 2020, the coronavirus pandemic Covid-19 has become a nightmare for people breathing. People quickly infected each other, filled hospitals, many people got sick, there were deaths. The remedy was that human interaction should be minimized and social distance rules must be followed. Travels between countries were stopped, businesses were closed, people were advised to stay at their homes. Even mandatory retrictions were applied. After all these measures, the lockdowns were gradually eased in summer 2020, but Covit-19 is still active.

The returns from the last quarter of 2019 till so far, which we have summarized roughly, have not been surprising. It was known, lived and continues to be experienced. IMO 2020 is the product of an industry awareness. We have brutally betrayed our world. IMO 2020 set out with strict rules to fulfill its duty. And he succeeded in that.

The crashes that came with Covid-19 proved how much harm the emissions caused to all living things in the world. In the process, data on pollution in the atmosphere dropped tremendously. Locks increase again as they are eased.

These deadlocks have dropped global oil demand. The leading oil producers, exporters, and importers of the world, which have fallen into each other, have suddenly entered into a friendly, cooperative, attitude and attitude to increase demand.

So lessons had to be learned!

Covid-19 and demand concerns remain, crude oil and distillate prices are still falling. IMO 2020 has reached its goals, it is no longer a scapegoat.

This article was written on 10/09/2020 and the technical figures, past analysis and forecasts may change in the future.