The Incoterms or International Commercial Terms are a series of pre-defined commercial terms published by the International Chamber of Commerce (ICC) relating to international commercial law. They are widely used in international commercial transactions or procurement processes and their use is encouraged by trade councils, courts and international lawyers. A series of three-letter trade terms related to common contractual sales practices, the Incoterms rules are intended primarily to clearly communicate the tasks, costs, and risks associated with the global or international transportation and delivery of goods. Incoterms inform sales contracts defining respective obligations, costs, and risks involved in the delivery of goods from the seller to the buyer, but they do not themselves conclude a contract, determine the price payable, currency or credit terms, govern contract law or define where title to goods transfers.

The Incoterms rules are accepted by governments, legal authorities, and practitioners worldwide for the interpretation of most commonly used terms in international trade. They are intended to reduce or remove altogether uncertainties arising from the differing interpretations of the rules in different countries. As such they are regularly incorporated into sales contracts worldwide.

“Incoterms” is a registered trademark of the ICC.

The first work published by the ICC on international trade terms was issued in 1923, with the first edition known as Incoterms published in 1936. The Incoterms rules were amended in 1953,1967, 1976, 1980, 1990, 2000, and 2010 with the ninth version Incoterms 2020 having been published on September 10, 2019.

Incoterms 2020

Incoterms 2020 is the ninth set of international contract terms published by the International Chamber of Commerce, with the first set having been published in 1936. Incoterms 2020 defines 11 rules, the same number as defined by Incoterms 2010. One rule of the 2010 version (“Delivered at Terminal”; DAT) was removed, and is replaced by a new rule (“Delivered at Place Unloaded”; DPU) in the 2020 rules.

The insurance to be provided under terms CIF and CIP has also changed, increasing from Institute Cargo Clauses(C) to Institute Cargo Clauses(A). Under the CIF Incoterms® rule, which is reserved for use in maritime trade and is often used in commodity trading, the Institute Cargo Clauses (C) remains the default level of coverage, giving parties the option to agree to a higher level of insurance cover. Taking into account feedback from global users, the CIP Incoterms® rule now requires a higher level of cover, compliant with the Institute Cargo Clauses (A) or similar clauses.

In prior versions, the rules were divided into four categories, but the 11 pre-defined terms of Incoterms 2020 are subdivided into two categories based only on method of delivery. The larger group of seven rules may be used regardless of the method of transport, with the smaller group of four being applicable only to sales that solely involve transportation by water where the condition of the goods can be verified at the point of loading on board ship. They are therefore not to be used for containerized freight, other combined transport methods, or for transport by road, air or rail.

Incoterms 2020 also formally defines delivery. Previously, the term had been defined informally but it is now defined as the point in the transaction where “the risk of loss or damage passes from the seller to the buyer”.

Incoterms in government regulations

In some jurisdictions, the duty costs of the goods may be calculated against a specific Incoterm: for example in India, duty is calculated against the CIF value of the goods, and in South Africa the duty is calculated against the FOB value of the goods. Because of this it is common for contracts for exports to these countries to use these Incoterms, even when they are not suitable for the chosen mode of transport. If this is the case then great care must be exercised to ensure that the points at which costs and risks pass are clarified with the customer.

Rules for any mode of transport

EXW – Ex Works (named place of delivery)

The seller makes the goods available at their premises, or at another named place. This term places the maximum obligation on the buyer and minimum obligations on the seller. The Ex Works term is often used while making an initial quotation for the sale of goods without any costs included.

EXW means that a buyer incurs the risks for bringing the goods to their final destination. Either the seller does not load the goods on collecting vehicles and does not clear them for export, or if the seller does load the goods, they do so at buyer’s risk and cost. If the parties agree that the seller should be responsible for the loading of the goods on departure and to bear the risk and all costs of such loading, this must be made clear by adding explicit wording to this effect in the contract of sale.

FCA – Free Carrier (named place of delivery)

The seller delivers the goods, cleared for export, at a named place (possibly including the seller’s own premises). The goods can be delivered to a carrier nominated by the buyer, or to another party nominated by the buyer.

In many respects this Incoterm has replaced FOB in modern usage, although the critical point at which the risk passes moves from loading aboard the vessel to the named place. The chosen place of delivery affects the obligations of loading and unloading the goods at that place.

CPT – Carriage Paid To (named place of destination)

CPT replaces the C&F (cost and freight) and CFR terms for all shipping modes outside of non-containerized seafreight.

The seller pays for the carriage of the goods up to the named place of destination. However, the goods are considered to be delivered when the goods have been handed over to the first or main carrier, so that the risk transfers to buyer upon handing goods over to that carrier at the place of shipment in the country of Export.

CIP – Carriage and Insurance Paid to (named place of destination)

This term is broadly similar to the above CPT term, with the exception that the seller is required to obtain insurance for the goods while in transit. CIP requires the seller to insure the goods for 110% of the contract value under Institute Cargo Clauses (A) of the Institute of London Underwriters (which is a change from Incoterms 2010 where the minimum was Institute Cargo Clauses (C)), or any similar set of clauses, unless specifically agreed by both parties. The policy should be in the same currency as the contract, and should allow the buyer, the seller, and anyone else with an insurable interest in the goods to be able to make a claim.

CIP can be used for all modes of transport, whereas the Incoterm CIF should only be used for non-containerized sea-freight.

DPU – Delivered At Place Unloaded (named place of destination)

This Incoterm requires that the seller delivers the goods, unloaded, at the named place of destination. The seller covers all the costs of transport (export fees, carriage, unloading from main carrier at destination port and destination port charges) and assumes all risk until arrival at the destination port or terminal.

The terminal can be a Port, Airport, or inland freight interchange, but must be a facility with the capability to receive the shipment. If the seller is not able to organize unloading, they should consider shipping under DAP terms instead.

All charges after unloading (for example, Import duty, taxes, customs and on-carriage) are to be borne by buyer. However, it is important to note that any delay or demurrage charges at the terminal will generally be for the seller’s account.

DAP – Delivered At Place (named place of destination)

Incoterms 2010 defines DAP as ‘Delivered at Place’ – the seller delivers when the goods are placed at the disposal of the buyer on the arriving means of transport ready for unloading at the named place of destination. Under DAP terms, the risk passes from seller to buyer from the point of destination mentioned in the contract of delivery.

Once goods are ready for shipment, the necessary packing is carried out by the seller at their own cost, so that the goods reach their final destination safely. All necessary legal formalities in the exporting country are completed by the seller at their own cost and risk to clear the goods for export.

After arrival of the goods in the country of destination, the customs clearance in the importing country needs to be completed by the buyer, e.g. import permit, documents required by customs and etc., including all customs duties and taxes.

Under DAP terms, all carriage expenses with any terminal expenses are paid by seller up to the agreed destination point. The necessary unloading cost at final destination has to be borne by buyer under DAP terms.

DDP – Delivered Duty Paid (named place of destination)

Seller is responsible for delivering the goods to the named place in the country of the buyer, and pays all costs in bringing the goods to the destination including import duties and taxes. The seller is not responsible for unloading. This term is often used in place of the non-Incoterm “Free In Store (FIS)”. This term places the maximum obligations on the seller and minimum obligations on the buyer. No risk or responsibility is transferred to the buyer until delivery of the goods at the named place of destination.

The most important consideration for DDP terms is that the seller is responsible for clearing the goods through customs in the buyer’s country, including both paying the duties and taxes, and obtaining the necessary authorizations and registrations from the authorities in that country. Unless the rules and regulations in the buyer’s country are very well understood, DDP terms can be a very big risk both in terms of delays and in unforeseen extra costs, and should be used with caution.

Rules for sea and inland waterway transport

The four rules defined by Incoterms 2010 for international trade where transportation is entirely conducted by water are as per the below. It is important to note that these terms are generally not suitable for shipments in shipping containers; the point at which risk and responsibility for the goods passes is when the goods are loaded on board the ship, and if the goods are sealed into a shipping container it is impossible to verify the condition of the goods at this point.

Also of note is that the point at which risk passes under these terms has shifted from previous editions of Incoterms, where the risk passed at the ship’s rail.

FAS – Free Alongside Ship (named port of shipment)

The seller delivers when the goods are placed alongside the buyer’s vessel at the named port of shipment. This means that the buyer has to bear all costs and risks of loss of or damage to the goods from that moment. The FAS term requires the seller to clear the goods for export, which is a reversal from previous Incoterms versions that required the buyer to arrange for export clearance. However, if the parties wish the buyer to clear the goods for export, this should be made clear by adding explicit wording to this effect in the contract of sale. This term should be used only for non-containerized seafreight and inland waterway transport.

FOB – Free on Board (named port of shipment)

Under FOB terms the seller bears all costs and risks up to the point the goods are loaded on board the vessel. The seller’s responsibility does not end at that point unless the goods are “appropriated to the contract” that is, they are “clearly set aside or otherwise identified as the contract goods”. Therefore, FOB contract requires a seller to deliver goods on board a vessel that is to be designated by the buyer in a manner customary at the particular port. In this case, the seller must also arrange for export clearance. On the other hand, the buyer pays cost of marine freight transportation, bill of lading fees, insurance, unloading and transportation cost from the arrival port to destination. Since Incoterms 1980 introduced the Incoterm FCA, FOB should only be used for non-containerized seafreight and inland waterway transport. However, FOB is commonly used incorrectly for all modes of transport despite the contractual risks that this can introduce. In some common law countries such as the United States of America, FOB is not only connected with the carriage of goods by sea but also used for inland carriage aboard any “vessel, car or other vehicle.”

CFR – Cost and Freight (named port of destination)

The seller pays for the carriage of the goods up to the named port of destination. Risk transfers to buyer when the goods have been loaded on board the ship in the country of Export. The Shipper is responsible for origin costs including export clearance and freight costs for carriage to named port. The shipper is not responsible for delivery to the final destination from the port (generally the buyer’s facilities), or for buying insurance. If the buyer requires the seller to obtain insurance, the Incoterm CIF should be considered. CFR should only be used for non-containerized seafreight and inland waterway transport; for all other modes of transport it should be replaced with CPT.

CIF – Cost, Insurance & Freight (named port of destination)

This term is broadly similar to the above CFR term, with the exception that the seller is required to obtain insurance for the goods while in transit. CIP requires the seller to insure the goods for 110% of the contract value under Institute Cargo Clauses (A) of the Institute of London Underwriters (which is a change from Incoterms 2010 where the minimum was Institute Cargo Clauses (C)), or any similar set of clauses, unless specifically agreed by both parties. The policy should be in the same currency as the contract. The seller must also turn over documents necessary, to obtain the goods from the carrier or to assert claim against an insurer to the buyer. The documents include (as a minimum) the invoice, the insurance policy, and the bill of lading. These three documents represent the cost, insurance, and freight of CIF. The seller’s obligation ends when the documents are handed over to the buyer. Then, the buyer has to pay at the agreed price. Another point to consider is that CIF should only be used for non-containerized sea freight; for all other modes of transport it should be replaced with CIP.

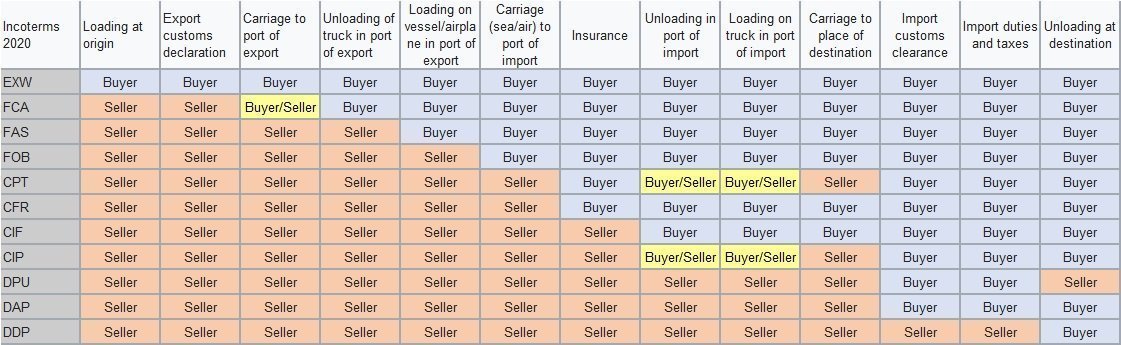

Allocations of costs to buyer/seller according to Incoterms 2020

All the information given in this article is written in good faith and the accuracy of any information in the article content is not guaranteed by the Bunkerist.